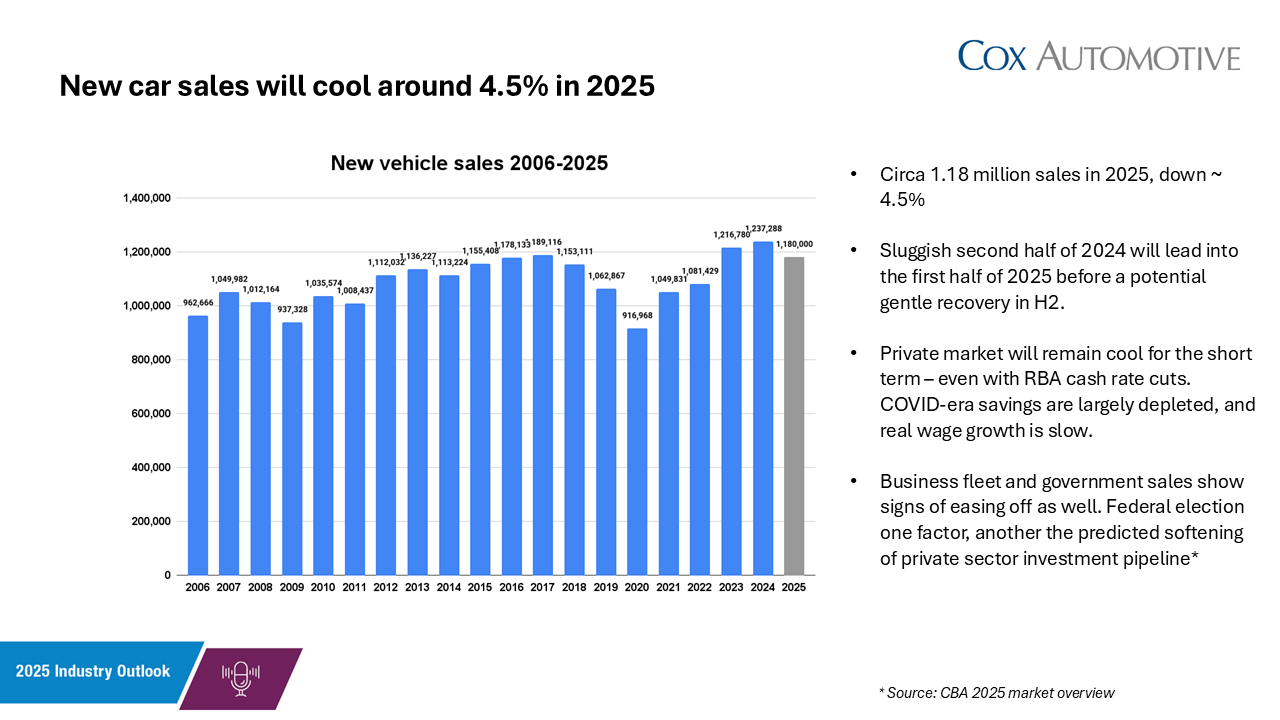

- Total sales expected to cool against 2024 record by around 5%, to ~ 1.18 million units.

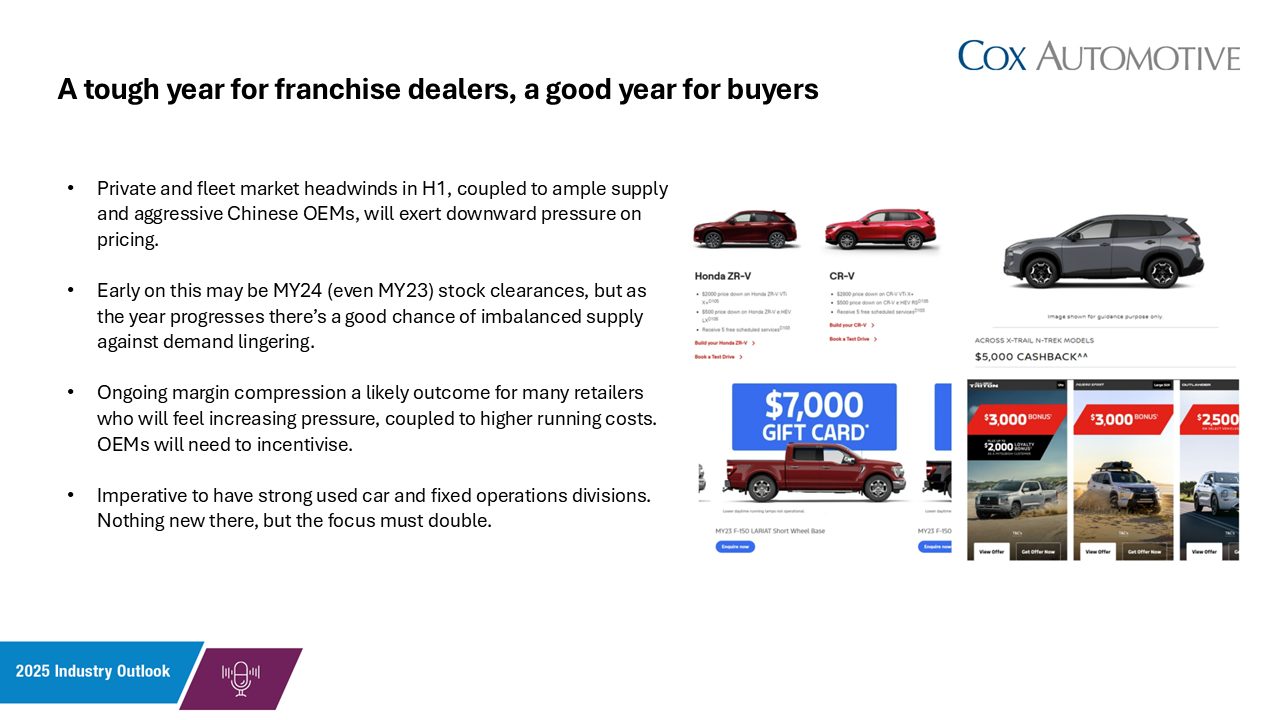

- Excess supply and lower private demand increase likelihood of discounting.

- Chinese brands e.g. BYD and MG to take market share to nearly 20%.

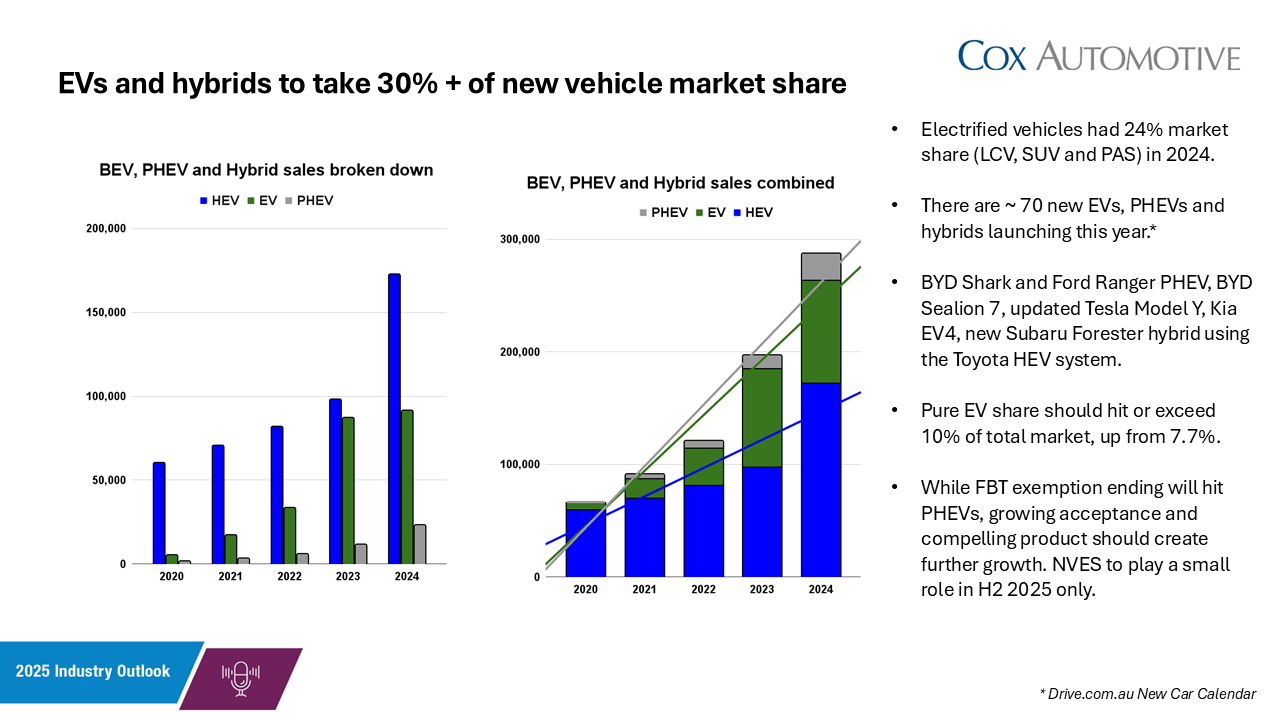

- ‘Electrified’ vehicles including hybrids and EVs to take ~ 30% market share.

- H2 likely to be stronger than H1, pending forecast Reserve Bank interest rate cuts.

Prospective new car buyers battling cost-of-living pressures can expect more affordable choices in 2025, with incentives and discounting expected to ramp up again this year.

Growing manufacturer inventory and even more intense market competition, coupled with presently slowing household demand for new vehicles, means 2025 will continue to offer up a ‘buyer’s market’ – unlike the supply constrained ‘seller’s market’ we saw during 2021-2023.

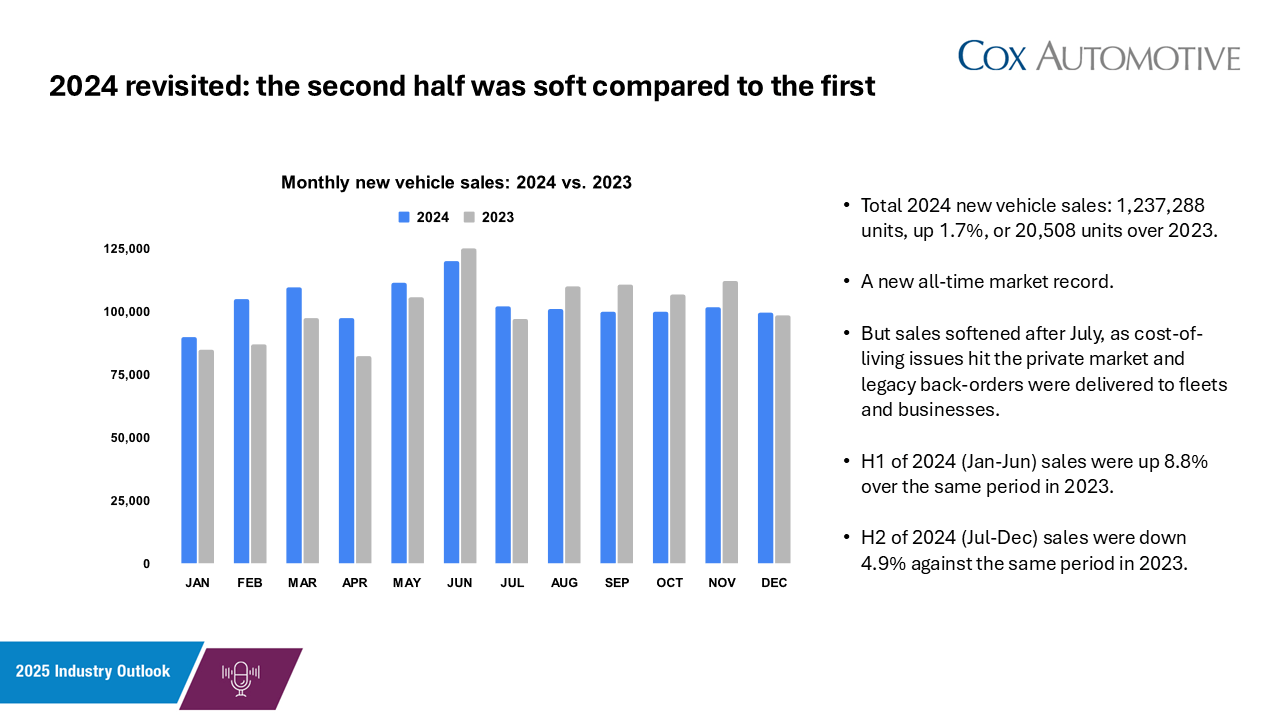

Forecast new vehicle sales for this year are around 1.18 million units according to vehicle services and market intelligence firm Cox Automotive Australia (CAA), down 4.6% over 2024’s all-time record tally of 1,237,288 vehicles, which was driven by the first half of last year.

In all likelihood, both private and fleet sales will face headwinds and cool year-on-year in the first half of 2025 in particular, driving the introduction of more incentives at OEM and dealer level to ‘move metal’ – manifesting as discounts or lower finance interest rates.

One key indicator of what 2025 holds is to monitor how the calendar year 2024 finished, and how that is expected to spill over into this year. Namely, 2024 was a year of two halves, with very strong growth in the first half (H1) of 8.8% but slowing sales in the second half (H2), down 4.9%.

The wider industry, including CAA, compares year-on-year figures for H1 and H2 (H1 of 2024 vs H1 of 2023, H2 of 2024 vs H2 of 2023) due to predictable seasonal trends in the market, giving a clearer view of what’s really going on. This scenario is no different.

Sales generally softened after June 2024 due to myriad factors, arguably the top one being a sluggish private market driven by reduced household discretionary spending amidst well-publicised cost-of-living pressures, low wage growth, and reduced COVID-era legacy savings.

Private vehicle sales – meaning any non-business, government or rental fleet purchase – decreased a substantial 8.0% across H2 2024, and CAA expects the structural factors driving this to linger into the first half of 2025 at least.

At the same time, while business and government fleet sales were strong early in 2024 in part because of better vehicle supply, allowing these large-scale buyers to turn over fleets they were forced to retain amidst the COVID-era shortages, they too cooled by 1.3% in H2.

Other factors that could impact non-private sales in 2025 include a predicted slowdown in the private investment pipeline*, and the predicted short-term impact in the lead up to the Federal Election.

Two further big-picture factors are expected to significantly impact the market in 2025, namely a predicted increase in electric vehicle (EV) sales after a sluggish 2024 (in which sales were up 4.7%), and a further dramatic expansion of offerings from Chinese domestic manufacturers.

CAA expects pure EV market share to increase from 7.7% across 2024** (91,292 sales) to around 10% of the market (around 115,000 sales), with BYD Australia set to be a significant factor alongside incumbent leader Tesla with its updated Model Y.

Meanwhile electrified vehicles – EVs, plug-in hybrids (PHEVs) and hybrids – are expected to take close to one-third of the market combined, up from 24% share across 2024. While hybrid leader Toyota is forecasting slightly lower sales, there are increasing numbers of competitors poised.

One thing to watch is the impact of the end of fringe-benefits tax concessions for leased PHEVs, which has been a huge factor in their steep recent sales growth. However, the rollout of PHEV utes such as the BYD Shark and Ford Ranger should grow the market despite the headwinds.

Australians are also going to buy more and more cars from China’s domestic manufacturers, with this market a low-barrier and lucrative destination in an era of increasing protectionism in the US and Europe. They undercut their competitors and are improving rapidly.

Chinese brands – namely MG, GWM, BYD, LDV and Chery – combined for about 142,000 Australian sales in 2024, equal to 12% market share. This year CAA expects share from Chinese marques to grow appreciably and potentially nudge 20%, one-in-five sales.

This year will see all those existing volume brands expand their line-ups significantly with promised new models, while a spate of new OEMs such as Geely and Leapmotor will arrive, with experienced management, factory backing, and engaged franchise dealer networks.

Chinese model launches will include the BYD Shark and Sealion 7 EV; Chery Tiggo 9 and Jaecoo J7 SUVs; LDV eTerron 9 electric ute; MG ES5 EV and HS hybrids; GWM Haval H7; Geely EX5; and Leapmotor C10, plus there will be growth from newcomers such as Zeekr, Deepal and JAC.

By the end of 2025, there will be around 15 Chinese brand names in the market, covering all segments and fuel types, with price bands from $25,000 and into six-figures.

“As cost-of-living pressures continue to impact the private market, and with supply no longer an overarching problem, you can expect to see an even harder-fought sector in 2025, with keener pricing and finance options a likely result for private and fleet buyers,” said Cox Automotive Australia CEO Stephen Lester.

“Big picture issues to watch include the Federal Election in April or May, the introduction of the New Vehicle Efficiency Standard, the end of Fringe Benefits Tax concessions for PHEVs, predicted cash rate cuts from the Reserve Bank of Australia, and the ongoing increase in volume from Chinese domestic brands, which captured 12% market share last year.

“We’re predicting a slight decline in volume this year, and more margin pressure for retailers.”

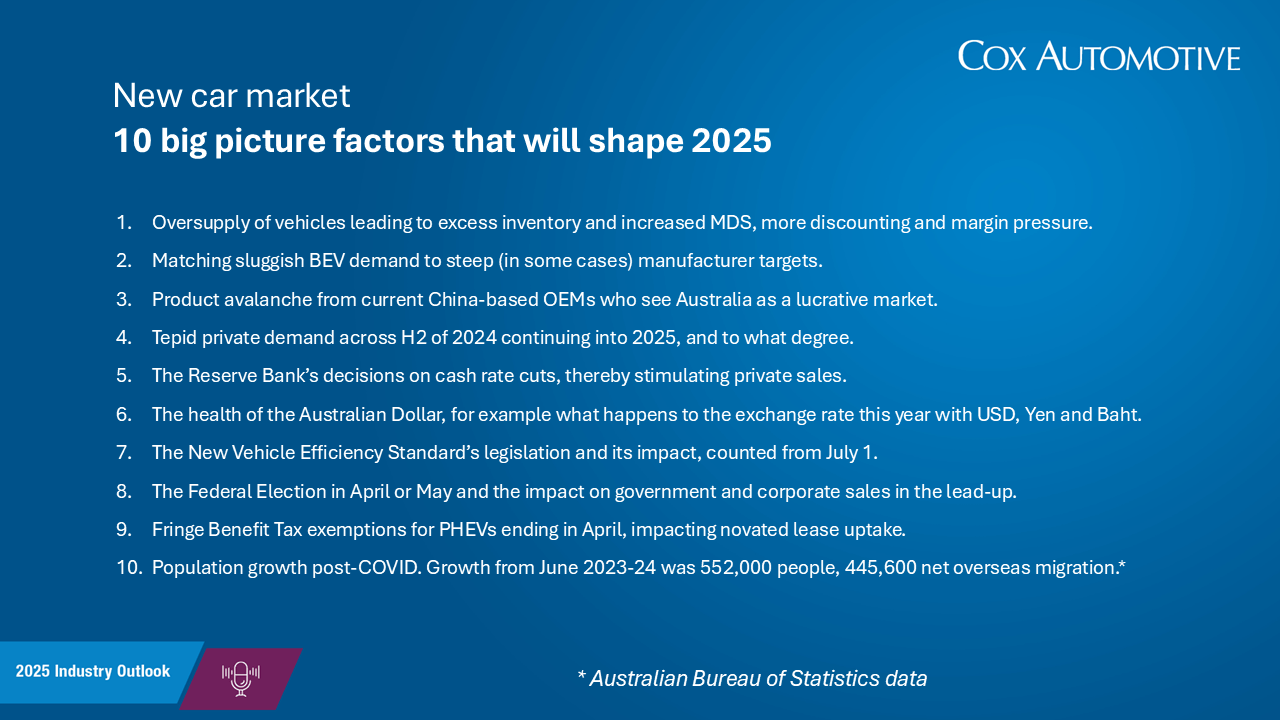

10 big picture factors that will shape the 2025 new car market:

-

- Oversupply of vehicles leading to excess inventory and increased days’ supply, more discounting and margin pressure at a dealer level, coupled with more manufacturer incentives.

- Matching sluggish BEV demand to steepening manufacturer targets and ongoing market fragmentation.

- The impending product avalanche from China-based OEMs that see Australia as a lucrative market.

- Comparatively tepid private demand across H2 of 2024 continuing into 2025 due to cost-of-living increases and a reduction in household COVID-era savings.

- The Reserve Bank’s decisions on cash rate cuts, which will eventually liberate more household discretionary spending and give the private market a push.

- The health of the Australian Dollar, for example what happens to the exchange rate this year with the USD, Japanese Yen, and Thai Baht.

- The New Vehicle Efficiency Standard’s legislation and its impact, which is not expected to bite too deep until 2026 and beyond when the targets ramp up.

- The Federal Election in April or May and the impact on government and corporate sales in the lead-up, as well as afterwards depending on business and consumer sentiment.

- Fringe Benefit Tax exemptions for PHEVs ending in April, impacting novated lease uptake, offset by the rollout of plug-in hybrid light commercial utes and vans.

- Steeper-than-average population growth post-COVID increasing the buyer pool. There are now more than 27 million people calling Australia home – a jump of 1 million people in less than two years thanks in part to post-pandemic overseas migration***.

> Download PDF

* Source: Commonwealth Bank Economic Insights 2025.

** Passenger, SUV and light commercial market, excludes Heavy Commercials.

*** Source: The Guardian reporting Australian Bureau of Statistics data.

About Cox Automotive:

Cox Automotive Australia is a full subsidiary of Atlanta-based Cox Automotive Inc, the world’s largest end-to-end vehicle services company.

In Australia the company owns Manheim auctions, which sells cars, heavy commercials and salvage all over the country, on behalf of fleets, governments, business, OEMs, insurers, financiers and more.

Cox Automotive Australia also makes and supports an array of retail software solutions including dealer websites (Radius), customer lead management (LeadDriver), inventory management (SmartPublisher), valuations (Kelley Blue Book), and service department customer experience (Xtime).

The company has more than 500 staff in Australia and New Zealand, with major offices in Melbourne and Brisbane, and sites in Sydney, Perth, Adelaide, Hobart, Darwin, Newcastle, Townsville, Auckland, and Christchurch.